Understand The New Executive Condominium Scheme and Why Timing Matters Now

If you have been quietly watching the Executive Condominium (EC) market and waiting for the right moment to make your move, that moment is now, and it may be closing faster than you think.

On 8 May 2026, Singapore’s Ministry of National Development announced its most sweeping overhaul of the EC housing scheme in over a decade. If you are an HDB upgrader who has been sitting on the fence, understanding what is disappearing and why could save you hundreds of thousands of dollars.

What Has Changed and Why It Matters

- The Minimum Occupation Period (MOP) Has Been Doubled

The Minimum Occupation Period for new Executive Condominiums has been doubled from 5 years to 10 years. If you buy a new EC launched under the revised scheme, you will need to live in it for a full decade before you can sell it to fellow Singaporeans or Permanent Residents, and only after 15 years will you be free to sell to any buyer, including foreigners.

Between 2021 and 2025, approximately 75% of ECs were sold by owners within five years of hitting their Minimum Occupation Period, up sharply from 45% in the preceding five-year period. Too many buyers were treating ECs as short-term investments rather than long-term homes, which drove prices up and squeezed genuine first-time buyers out of the market.

- More Units Reserved for First-Time Buyers

The first-timer quota at launch has been raised from 70% to 90%, with the priority window extended to 2 years. 9 out of every 10 units at a new EC launch will be reserved for buyers who have never owned a subsidised flat before, dramatically reducing competition from second-time buyers who typically carry larger cash reserves.

- The Deferred Payment Scheme Has Been Abolished

The Deferred Payment Scheme has been abolished, and all buyers must now use the Normal Progressive Payment Schedule. This is the change with the greatest immediate financial impact on HDB upgraders, and it is the one you need to understand most urgently.

Understanding Your Payment Options: Normal vs Deferred

The Normal Progressive Payment Scheme

Under the Normal Progressive Payment Scheme, your payments are tied to the construction milestones of your EC unit:

- 5% — Booking fee upon exercising the Option to Purchase

- 15% — Upon signing the Sales and Purchase Agreement (total upfront: 20%)

- 5% — Upon completion of foundation works

- Remaining balance — Progressively via bank loan as construction milestones are reached

Once you sign the Sales and Purchase Agreement, your bank loan kicks in progressively alongside construction. For HDB flat owners, this means servicing your EC mortgage while still paying for your existing HDB flat, a financial juggling act that requires careful planning.

The Deferred Payment Scheme: What It Was and Why It Helped

The Deferred Payment Scheme (DPS) was a lifeline designed for HDB upgraders who needed breathing room between buying their new EC and selling their existing flat:

- 5% — Booking fee upon exercising the Option to Purchase

- 15% — Upon signing the Sales and Purchase Agreement (total: 20%)

- No further payments required until the developer announces the Temporary Occupation Period (TOP)

Under DPS, your bank loan did not begin until TOP, typically 3 to 5 years after purchase. This gave HDB upgraders a crucial window to continue living in their existing flat without a concurrent mortgage, time the sale of their HDB flat to coincide with TOP, and use those sales proceeds to cover the remaining 5% and reduce their overall loan.

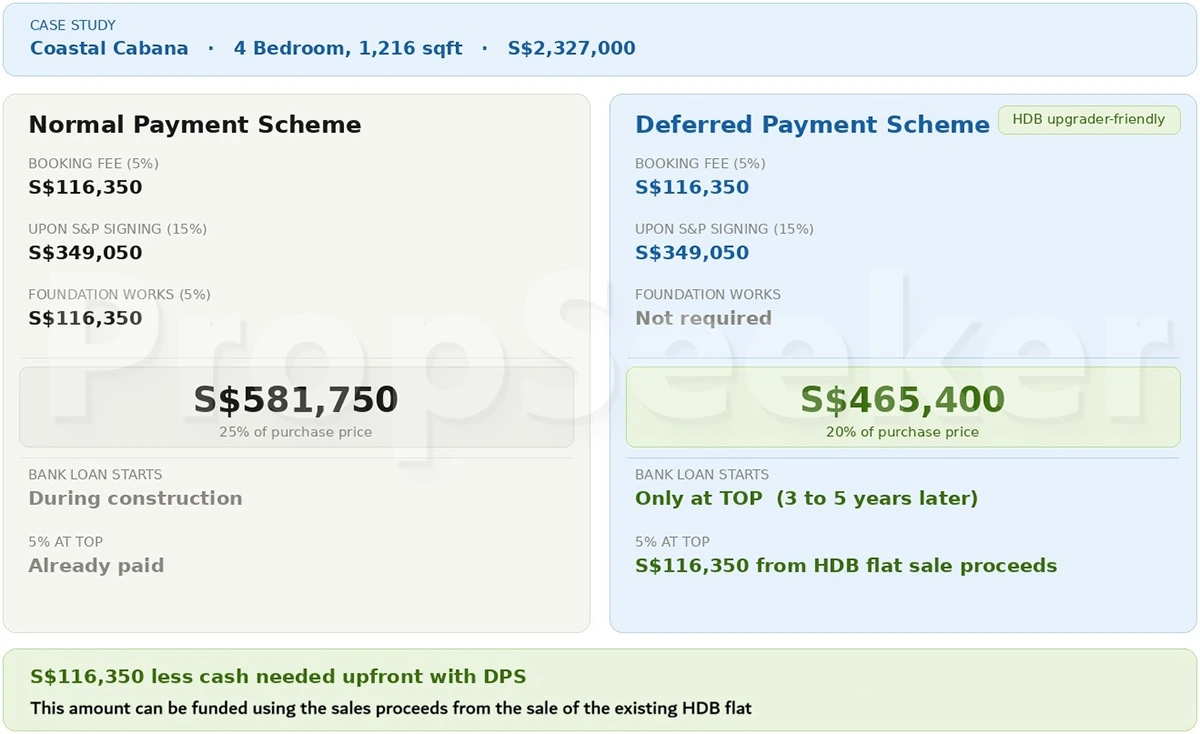

How the Deferred Payment Scheme Helped Real HDB Upgraders

Consider a 4-bedroom unit at Coastal Cabana, 1,216 square feet, sold at $2,327,000.

Under the Normal Payment Scheme, an upgrader would need to fork out $581,750 upfront from their cash and CPF savings, and that is before factoring in the bank loan instalments that begin during construction.

Under the Deferred Payment Scheme, the same upgrader would only need $465,400 upfront. The remaining $116,350 (5%) would only fall due at TOP, by which time they could have already sold their HDB flat and used the sales proceeds to fund this payment, essentially letting their old asset pay for their new one.

For many families, this $116,350 in cash flow relief spread over three to five years was the difference between being able to upgrade and being locked out of the EC market entirely.

What Happens Now That the DPS Is Gone?

HDB upgraders will face tighter cash flow pressure. Without the DPS buffer, buyers must manage both their existing HDB flat costs alongside progressive EC loan repayments during construction, placing a greater premium on financial readiness before committing.

The window to plan your upgrade narrows. The DPS allowed buyers to commit early and plan their HDB exit at their own pace. Under the Normal Payment Scheme, that timeline is more compressed and more dependent on your bank loan approval and CPF availability at the point of purchase.

Demand for existing EC projects under the old scheme will intensify. Since the new rules only apply to EC GLS tenders closing from 8 May 2026, projects already launched or on sites already tendered before that date are still operating under the original scheme, including the availability of the Deferred Payment Scheme.

Conclusion: A Closing Window You Cannot Afford to Ignore

As of May 2026, a select number of existing and upcoming Executive Condominiums are still operating under the original EC housing scheme, which means the Deferred Payment Scheme, the five-year MOP, and the more accessible payment structure that HDB upgraders have relied upon for years are still very much available on these projects.

Once these projects sell out or new tenders close, that window shuts permanently. There will be no more DPS, no more five-year MOP, and no more ability to time your HDB sale to fund your EC purchase at TOP.

If you want to know which Executive Condominiums are still running the existing scheme, contact us immediately before the new scheme kicks in.

Reach out to us today for a no-obligation consultation. We will walk you through which Executive Condominiums are still running the original scheme, whether DPS is still an option for you, and exactly how to structure your finances for a smooth and stress-free upgrade. Do not wait until these projects are gone.

Click below and get a Free consultation and Financial planning